China and the Iran War: Strategic Winner or Economic Casualty?

Short-term resilience meets long-term vulnerability as China navigates the economic fallout of the Iran war.

The ongoing conflict involving Iran has triggered a global energy shock, forcing major economies to reassess their strategic positions. Among them, China occupies a uniquely complex position. On the surface, Beijing appears well-prepared—benefiting from energy stockpiles, discounted access to oil, and geopolitical distance from direct conflict. Yet beneath this resilience lies a more fragile reality: the same war that offers short-term strategic advantages may also expose deeper economic vulnerabilities.

This raises a central question: Is China emerging as a quiet winner of the Iran war, or is it facing mounting economic risks?

Strategic Advantages: Energy Security and Geopolitical Leverage

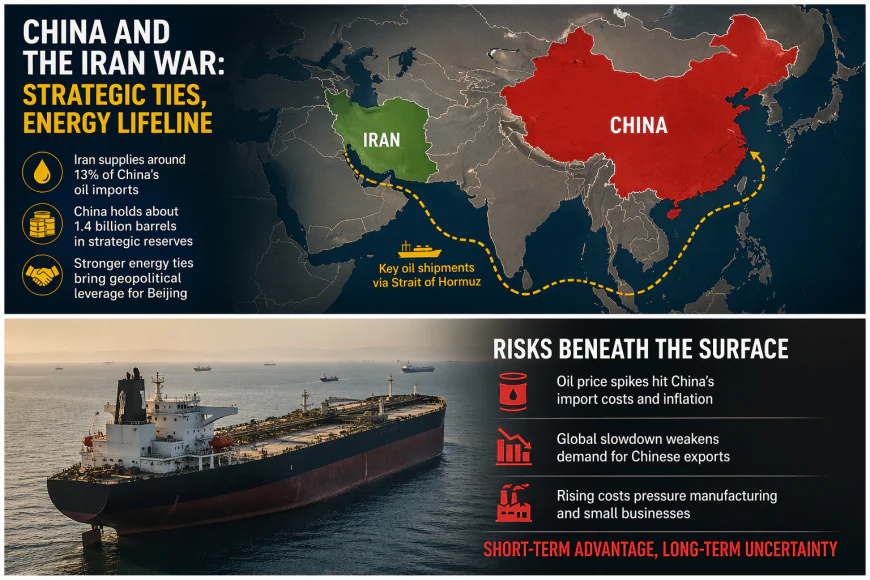

In the short term, China appears relatively well-positioned. One of the most significant advantages stems from its long-standing energy relationship with Iran. China has been importing discounted Iranian oil for years, with Iran accounting for around 13% of its oil imports under long-term agreements.

Crucially, Beijing anticipated geopolitical instability. By late 2025, it had accumulated an estimated 1.4 billion barrels of crude oil in strategic reserves, providing a buffer against supply disruptions. This stockpiling strategy has allowed China to avoid the immediate energy shocks experienced by many Western economies.

The war has also elevated China’s diplomatic profile. While avoiding direct military involvement, Beijing has positioned itself as a stabilising actor, engaging in behind-the-scenes diplomacy and encouraging negotiations. This reinforces China’s broader ambition to present itself as a responsible global power, particularly in contrast to perceived Western interventionism.

From a geopolitical perspective, the conflict may also indirectly benefit China by diverting U.S. attention and resources away from the Indo-Pacific region. This shift potentially reduces immediate pressure on China in areas such as Taiwan or the South China Sea, strengthening its strategic position.

Taken together, these factors suggest that China has entered the conflict from a position of relative preparedness, with both economic and geopolitical advantages.

Structural Vulnerabilities: Energy Dependence and Export Exposure

However, this apparent resilience masks deeper structural risks. Despite its stockpiles, China remains the world’s largest oil importer and is therefore highly sensitive to sustained increases in global energy prices.

According to economic modelling cited by Bruegel, a 25% rise in oil prices could reduce China’s GDP by approximately 0.5%. This highlights a key vulnerability: while China can absorb short-term shocks, prolonged price increases would have measurable macroeconomic consequences.

The war has already triggered volatility in global energy markets. Oil prices surged sharply following the outbreak of conflict, with broader economic effects including rising inflation and production costs worldwide. For China, this translates into higher input costs across its vast manufacturing sector.

There are early signs of strain. While China recorded around 5% GDP growth in early 2026, underlying pressures are intensifying. Export growth has slowed, and small and medium-sized enterprises—responsible for roughly 80% of urban employment—are facing rising costs and declining demand.

This reflects a critical point emphasised in the Bruegel analysis: China’s vulnerability is not limited to energy supply, but extends to external demand. As the global economy weakens under the weight of higher energy prices and geopolitical uncertainty, demand for Chinese exports is likely to decline.

In other words, even if China secures sufficient energy, it may struggle to sustain growth if its key export markets contract.

The Global Transmission Mechanism: From War to Economic Slowdown

The Iran war illustrates how geopolitical shocks propagate through the global economy. The primary transmission channel is energy. Disruptions in the Strait of Hormuz—through which a significant share of global oil supply flows—have raised fears of supply shortages, driving up prices and increasing volatility.

For China, the effects are both direct and indirect. Directly, higher oil prices increase production and transportation costs. Indirectly, they contribute to global inflation, which in turn reduces consumer demand in key export markets such as Europe and the United States.

Recent forecasts suggest that while China’s economy showed signs of recovery in early 2026, the war has “jolted” its outlook, introducing new uncertainty and downside risks.

This dual impact—rising costs at home and weakening demand abroad—creates a difficult environment for sustained growth. It also exposes the limitations of China’s economic model, which remains heavily reliant on manufacturing and exports despite efforts to rebalance toward domestic consumption.

Resilience Strategies: Diversification and Self-Reliance

China is not passive in the face of these risks. Policymakers have already begun implementing measures to mitigate the impact of the conflict. These include diversifying energy imports, increasing domestic production, and adjusting fuel pricing to stabilise domestic markets.

These actions align with China’s broader “dual circulation” strategy, which aims to reduce dependence on external markets while strengthening domestic demand and technological self-sufficiency.

In the short term, such strategies enhance resilience. China’s ability to maintain relative stability during the initial phase of the conflict suggests that its long-term planning has been effective. Indeed, some analysts argue that Beijing has coped better than expected, leveraging both economic preparation and diplomatic positioning.

However, resilience is not immunity. The effectiveness of these measures depends on the duration and intensity of the conflict. A prolonged war would likely strain even China’s substantial buffers.

A Conditional Advantage

China’s position in the Iran war cannot be reduced to a simple binary of winner or loser. In the short term, it has clear advantages. Strategic oil reserves, discounted imports, and diplomatic positioning have insulated it from the immediate shocks experienced by other economies.

Yet these advantages are conditional. Beneath the surface lies a set of structural vulnerabilities—particularly energy dependence and exposure to global demand—that could undermine China’s economic stability if the conflict persists.

Ultimately, China is best understood not as a clear winner, but as a strategic hedger. It has been prepared effectively for disruption and may even gain geopolitical influence in the process. However, its long-term economic trajectory remains tied to the same global system that the war is destabilising.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

I’m a freelance writer with a passion for business, lifestyle, and opinion pieces that explore culture, trends, and real-world insights. I bring a perspective that blends professional knowledge with cultural awareness, drawing on my experience in real estate and a keen interest in South Asian lifestyle and culture. I hold a Master’s in Popular Music Practice, and outside of writing, I enjoy playing the flute and reading about philosophy and psychology. I love crafting engaging, thought-provoking stories and am always excited to pitch fresh ideas or take on features that connect communities, trends, and the bigger picture.

Comments (0)